Throughout this blog, we have provided many insights into the key risks that business owners face on a daily basis, such as fires in industrial warehouses, pollution of the environment around production sites, catastrophic events, large product defect claims, workplace accidents and illnesses, food contamination and personal financial liability of directors.

In addition to these serious threats, there is the risk that our customers will not pay their invoices, exposing the company to financial consequences as serious as bankruptcy.

In this article we offer a summary of the benefits of trade credit insurance, followed by a further discussion of political and country risk at an international level.

When exporting abroad to distant countries, of which one is unfamiliar not only with the language but also with the legal system, customs and traditions, it is absolutely strategic assessing the creditworthiness of a business partner.

In addition to the risk of non-delivery, or even destruction, of the goods during transport (the case of the militiamen in Yemen is one of many examples we could give), there is also the possibility – once the goods have arrived at their destination – of non-payment of invoices.

Below we answer some of the key questions our clients ask us to help them understand how they can protect themselves before the sudden insolvency of a strategic supplier or the non-payment of invoices by several customers negatively impacts their company’s balance sheet.

‘Why is credit insurance still such an important tool for companies today?’

Businessmen know very well that insolvencies are on the rise globally, as are credit expiries.

The crisis that is mainly affecting the automotive and white goods industries at the moment, with the closure of factories and plants throughout Europe, is reverberating through the supply chain and does not make any difference between small, middle and large company: all suppliers of the large industrial groups are in trouble, being exposed to non-payment of orders and shipments that have already been processed.

Generally speaking, when we speak of trade credit risk, we are referring to the case where our supplier does not pay for goods, either because it has suddenly shut down its operations or because decides to defer payment of the invoice.

For our company this means, put very banally, one thing only: sudden liquidity crisis.

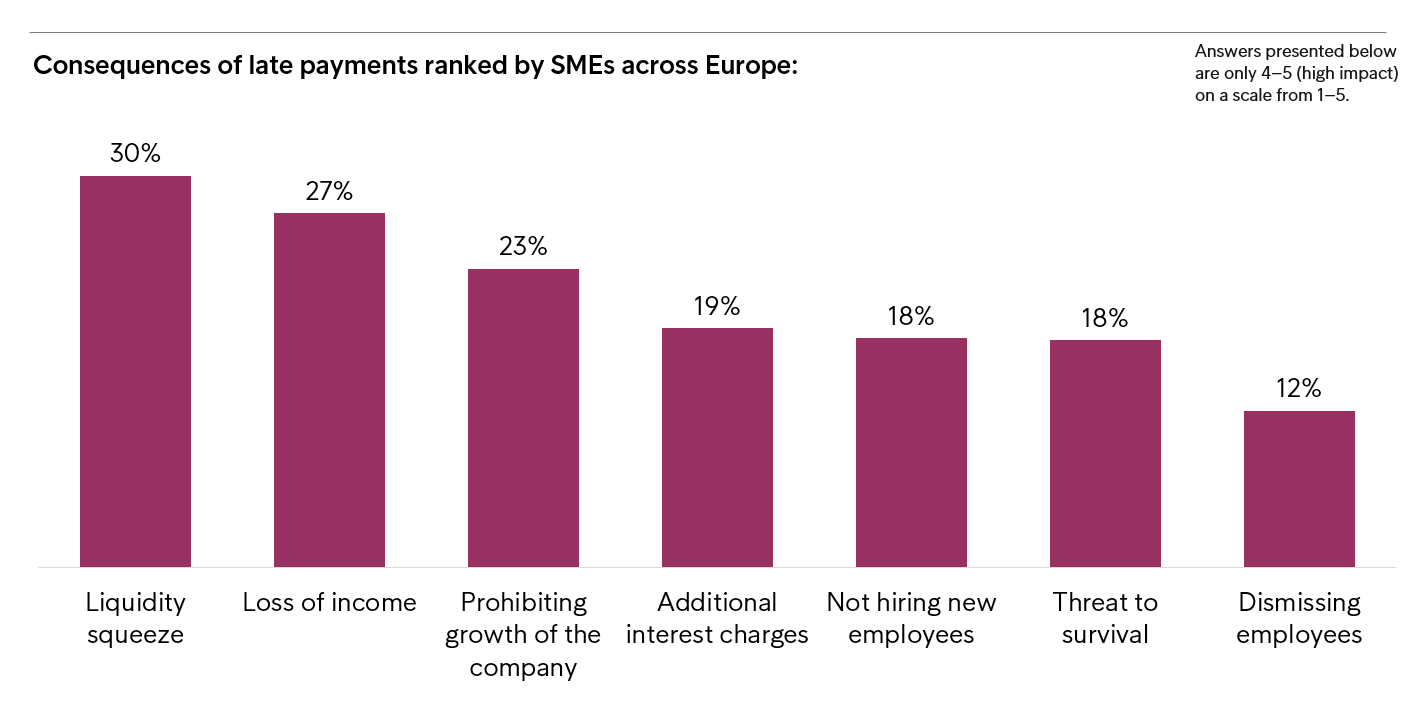

For the sake of clarity, here below you can find an interesting graph that summarises very clearly what consequences, both financial and employment-related, European companies face in the event of unpaid receivables.

To recapitulate, in the event of non-payment of invoices, there are three main financial consequences that can negatively have a direct impact on the balance sheet: in first place is an immediate liquidity crisis, followed by loss of turnover and the company’s inability to grow.

But beware: when the non-payment of receivables concerns a large number of suppliers, the company may even risk bankruptcy.

‘In addition to these risks, what other negative consequences do companies without credit insurance face?’

Let’s take a practical case: if our company plans to expand abroad by exporting its products, the sudden non-payment of an important invoice can literally knock the internationalisation project to the ground, thus opening the door to our competitors who can easily take over the market shares we thought we would make our own.

Another risk that cannot be overlooked is the limited freedom to plan industrial strategies: in the absence of credit insurance, entrepreneurs are very reluctant to invest in new markets with the necessary calmness and composure, knowing that the non-payment of an invoice by a new foreign customer can have a negative impact on the company’s finances.

So this insurance is a useful tool with which business owners are able to sell more products and services and to compete – if not on an equal footing with large corporations –certainly with companies similar in size with greater peace of mind.

‘Globally, which countries are most at risk?’

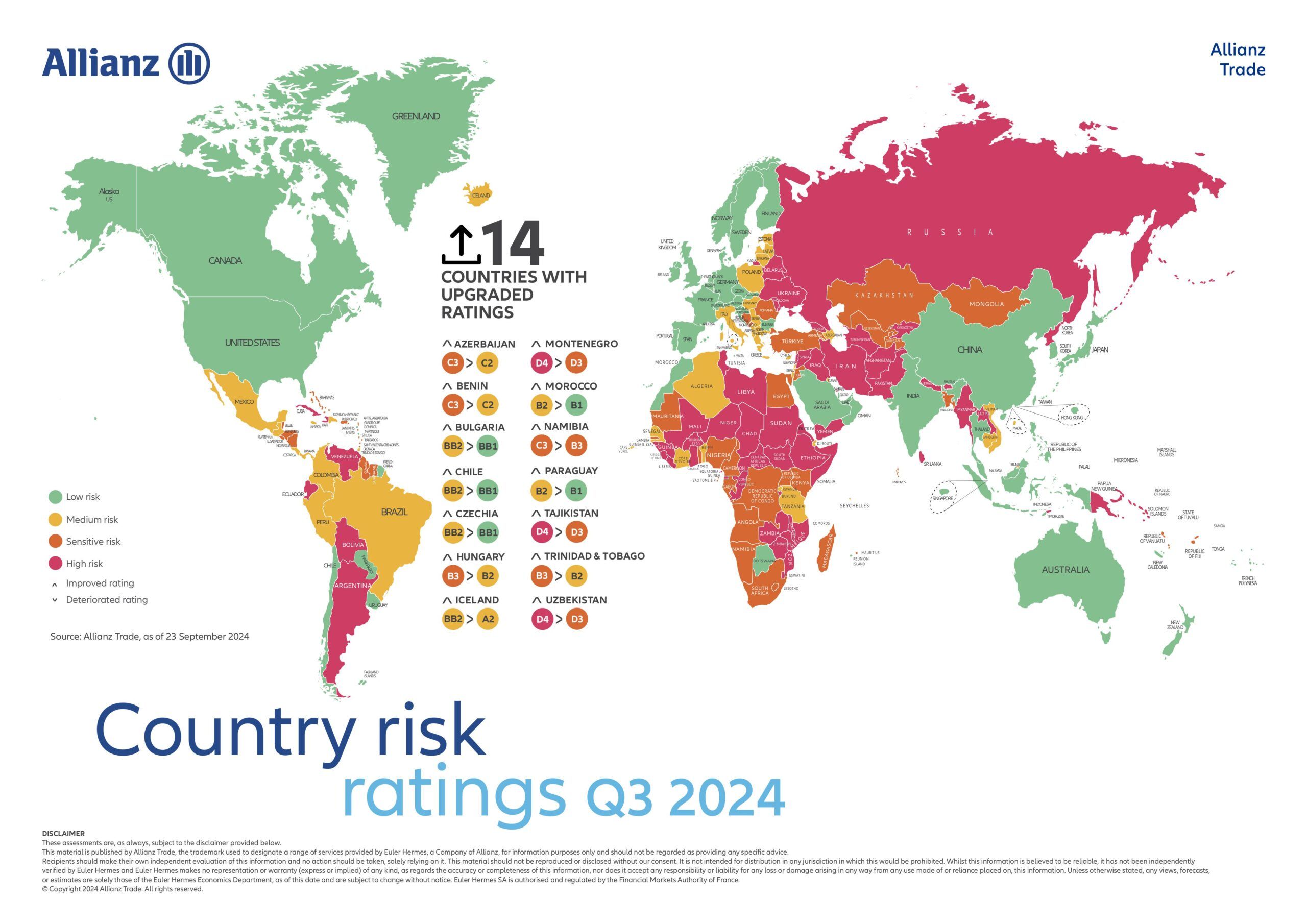

Insurance companies specialized in credit default insurance continually update their databases, offering their customers the possibility of monitoring the creditworthiness and political risk of the countries to which they decide to export.

In addition to this general information, summarised in the chart above, we advise companies to consult their insurance advisor specialising in these risks, in order to obtain further information on the financial health of the company they want to do business with and thus avoid nasty surprises.

‘We have just seen that the number of insolvencies is growing globally. With specific reference to the Visegrad region, do companies expect to face insolvencies of their customers?’

To date the situation is by no means dramatic, but it needs to be monitored very closely.

Almost 60 percent of companies in Central and Eastern Europe expect an increase in insolvencies in the coming year, especially in Romania and the Czech Republic and in the construction sector.

While 50% of companies expect no change in payment behaviour of B2B customers, with the agribusiness sector optimistic about an improvement, the negativity is most evident in the steel-metal sector.

We strongly suggest that companies keep up to date through the support of risk managers and insurance consultants who are familiar with credit and political risks on an international level.

‘Is credit insurance only for companies that export or also for those that only sell in the domestic market?’

Well, insurance companies offer commercial credit insurance in both cases.

With specific reference to export credit, i.e. international trade, the credit guarantee is insured for short or medium term credit together with the political risk (war, duties, cancellation of a contract…), to which we will speak about in another article.

‘Above we have set out, at a general level, the risks companies face in the event of non-payment of invoices: in a nutshell, what does trade credit insurance consist of?’

This insurance solution functions as a guarantee when customers are insolvent after payment of one or more invoices.

The insurance company, taking into account the reliability and financial stability of the customer portfolio, sets the maximum amount that can be indemnified in the event of insolvency for each customer.

During the insured year, the customer, supported by its risk managers and insurance consultants, receives a real tailor-made credit management service through the collection of information, analysis of records, verification and cross-checking of information, and study of financial statements.

In the event of non-payment, the insured may request payment of the indemnity within 30 days from the first communication to the company.

However, even before this communication, we would like to point out that the company may also choose to independently manage a possible negotiation with its supplier, setting a new time limit for the credit in order to protect business relations with customers.

‘Can I insure the credits of a single customer or is it necessary to put under coverage the entire portfolio?’

We have to make an important distinction between domestic and export credit.

In the first case, companies are required to insure the entire portfolio in its entirety, thus avoiding that only those customers to whom we have assigned a high default rate are included in the cover. In the second, it is possible to cover the individual international business transaction.

‘At the international level, what are the main types of credit insurance cover?’

International companies that have been operating for decades in the field of domestic and international commercial transactions provide with a detailed offer of credit management services and the issuance of ad hoc policies, tailored to the country, market and legislation where the company is located.

At a very general level, we can identify four types of cover, to guarantee the entire customer package, a specific segment of our clientele, a single large client/trade or against extremely large financial losses.

‘Besides credit insurance, are there alternatives?’

Absolutely. They are self-insurance, letter of credit or factoring.

These are all equally valid instruments for managing debt-credit relationships between companies, but they have, compared to commercial and political credit insurance, limitations that absolutely must be considered. We will discuss it in another article.

‘Are there cases in which a trade credit policy is not necessary?’

In my personal opinion, in relations between internationalised companies that are part of the same group, it may be redundant to insure the risk of non-payment of goods produced by the foreign subsidiary and purchased by the parent company.

Rather, there are other very serious financial consequences for the parent company if the foreign subsidiary, which has been completely destroyed by fire or flood, can no longer send the raw or semi-processed material to the mother company, in terms of contingent business interruption.

Who to rely on in order to reduce credit risks and protect our expansion projects abroad.

Who we can rely on to reduce credit risk and protect our overseas expansion projects.

In this article, we have illustrated at a very general level the financial risks that companies face in the event of non-payment of invoices by highlighting some of the main features of trade credit insurance.

However, even before purchasing this specific insurance solution, companies must pay close attention to prevention by constantly and closely monitoring the financial health of the customers to whom they sell their products and services, and by drawing up a proper credit risk mitigation plan.

The involvement of internationally experienced insurance consultants is strategic: they listen and guide us in reducing these risks before unpaid invoices, duties, sanctions, embargoes and exchange rate fluctuations in foreign and unknown countries jeopardise the internationalisation project in which we have invested our time and money.